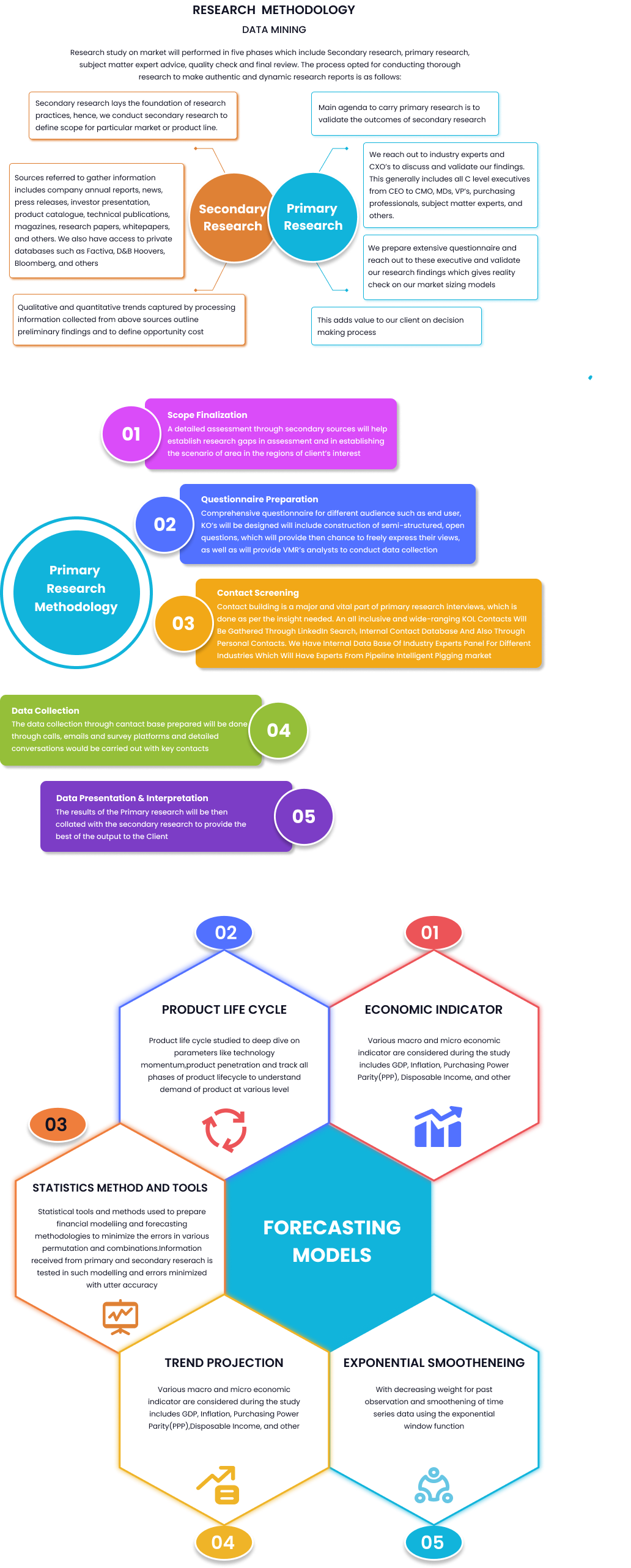

.png)

Global Semiconductor Bonder Market Size By Type (Wire Bonder, Die Bonder), By Application (Integrated Device Manufacturer (IDMs), Outsourced Semiconductor Assembly and Test (OSATs)), By Region, And Se...

Report Id: 12247 | Published Date: Feb 2023 | No. of Pages: | Base Year for Estimate: Feb 2023 | Format:

The Global Semiconductor Bonder Market was valued at USD 1.8 billion in 2023 and is projected to reach USD 3.5 billion by 2031, growing at a CAGR of 8.4% during the forecast period from 2023 to 2031. The rapid expansion of the semiconductor industry, fueled by increasing demand for consumer electronics, automotive chips, and advanced packaging technologies, is driving market growth. Semiconductor bonders are essential for integrated circuit (IC) packaging, allowing efficient and reliable chip interconnections in electronic devices. The increasing adoption of 3D IC packaging, miniaturized components, and advanced semiconductor manufacturing technologies is further propelling market expansion.

Drivers

1. Rising Demand for Advanced Packaging

Solutions

The semiconductor industry is witnessing a

shift towards advanced packaging techniques such as flip-chip bonding, 3D

stacking, and system-in-package (SiP). These technologies enhance device

performance, power efficiency, and miniaturization, boosting demand for

semiconductor bonders.

2. Growth in Consumer Electronics and

Automotive Industry

The proliferation of smartphones, tablets,

wearables, and electric vehicles (EVs) has increased the need for

high-performance chips. Automotive manufacturers are integrating ADAS (Advanced

Driver Assistance Systems), infotainment, and autonomous driving technologies,

requiring sophisticated semiconductor bonding solutions.

3. Expansion of AI, IoT, and 5G Networks

The deployment of 5G networks, artificial

intelligence (AI), and the Internet of Things (IoT) is driving the production

of high-performance semiconductor chips, necessitating precise and efficient

bonding technologies to improve chip connectivity and durability.

Restraints

1. High Initial Investment and Maintenance

Costs

Semiconductor bonding equipment requires

significant capital investment, making it challenging for small and mid-sized

semiconductor manufacturers to adopt the latest bonding technologies.

Additionally, maintenance and calibration costs add to operational expenses.

2. Supply Chain Disruptions and Material

Shortages

The semiconductor industry is highly

susceptible to supply chain disruptions, geopolitical tensions, and raw material

shortages. Delays in the supply of essential components, such as gold and

copper bonding wires, impact production efficiency and market growth.

Opportunities

1. Advancements in Wafer-Level and Hybrid

Bonding

Emerging wafer-level packaging and hybrid

bonding techniques are revolutionizing semiconductor manufacturing, enabling

smaller, faster, and more energy-efficient chips. Manufacturers investing in

these technologies can gain a competitive edge.

2. Expansion in Emerging Markets

Countries like China, India, and South

Korea are heavily investing in semiconductor fabrication plants (fabs) and chip

production facilities, creating significant growth opportunities for

semiconductor bonder manufacturers.

3. Integration of AI and Automation in

Bonding Processes

The incorporation of AI-driven automation,

robotics, and predictive analytics in semiconductor bonding processes is

improving production efficiency and yield rates, attracting investments in

automated bonding solutions.

Market by System Type Insights

Wire Bonder Segment Leading the Market

Wire bonders accounted for the largest

market share in 2023, driven by their cost-effectiveness and widespread

application in memory chips, RF devices, and power semiconductors. However,

flip-chip bonders are expected to grow at the highest CAGR due to their

advantages in high-performance computing, AI chips, and advanced packaging

solutions.

Market by End-use Insights

Consumer Electronics Segment Dominates

The consumer electronics segment held the

largest market share in 2023, attributed to increasing demand for smartphones,

tablets, laptops, and smart devices. Meanwhile, the automotive segment is

expected to witness the fastest growth, fueled by the adoption of EVs,

autonomous driving technologies, and smart vehicle components.

Market by Regional Insights

Asia-Pacific Leading the Market

Asia-Pacific dominated the market in 2023,

driven by the presence of major semiconductor manufacturers in China, Taiwan,

South Korea, and Japan. The region is home to leading semiconductor fabrication

plants (fabs) and packaging service providers, making it the most significant

contributor to market growth.

Meanwhile, North America is experiencing

strong growth, with major semiconductor companies such as Intel, Texas Instruments,

and NVIDIA investing in advanced packaging and semiconductor bonding

technologies. Europe is also witnessing growth, driven by increasing government

investments in semiconductor manufacturing and R&D initiatives.

Competitive Scenario

Key players in the Global Semiconductor

Bonder Market include:

Kulicke & Soffa Industries, Inc.

ASM Pacific Technology Ltd.

Besi (BE Semiconductor Industries N.V.)

Palomar Technologies

TPT Wire Bonder

Shinkawa Ltd.

F&K Delvotec Bondtechnik GmbH

Hesse GmbH

These companies are focusing on

technological innovations, partnerships, mergers & acquisitions, and

expanding manufacturing facilities to strengthen their market position.

Key

Market Developments

2023: Kulicke & Soffa launched its

latest high-speed hybrid bonding platform, improving throughput for advanced

semiconductor packaging.

2024: ASM Pacific Technology announced a

partnership with a leading semiconductor foundry to develop next-gen AI-driven

wire bonding solutions.

2025: Besi introduced an AI-based

predictive maintenance system for semiconductor bonders, reducing downtime and

improving production efficiency.

Scope

of Work – Global Semiconductor Bonder Market

|

Report

Metric |

Details |

|

Market Size in 2023 |

USD 1.8 billion |

|

Projected Market Size in 2031 |

USD 3.5 billion |

|

CAGR (2023-2031) |

8.4% |

|

Largest Market Segment by System Type |

Wire Bonder |

|

Largest Market Segment by End-use |

Consumer Electronics |

|

Leading Region |

Asia-Pacific |

|

Key Companies |

Kulicke & Soffa, ASM Pacific, Besi,

Palomar Technologies |

|

Market Drivers |

Growth in consumer electronics, expansion

of AI & 5G, rising demand for advanced packaging solutions |

|

Market Restraints |

High investment costs, supply chain

disruptions |

|

Market Opportunities |

Advancements in wafer-level packaging,

expansion in emerging markets, AI-driven automation in bonding processes |

Speak with an analyst to get exclusive insights tailored to your needs